Bidder¶

Market participating resources (e.g., generators, IESs) submit energy bids

(a.k.a., bid curves) to the day-ahead and real-time markets for each trading time

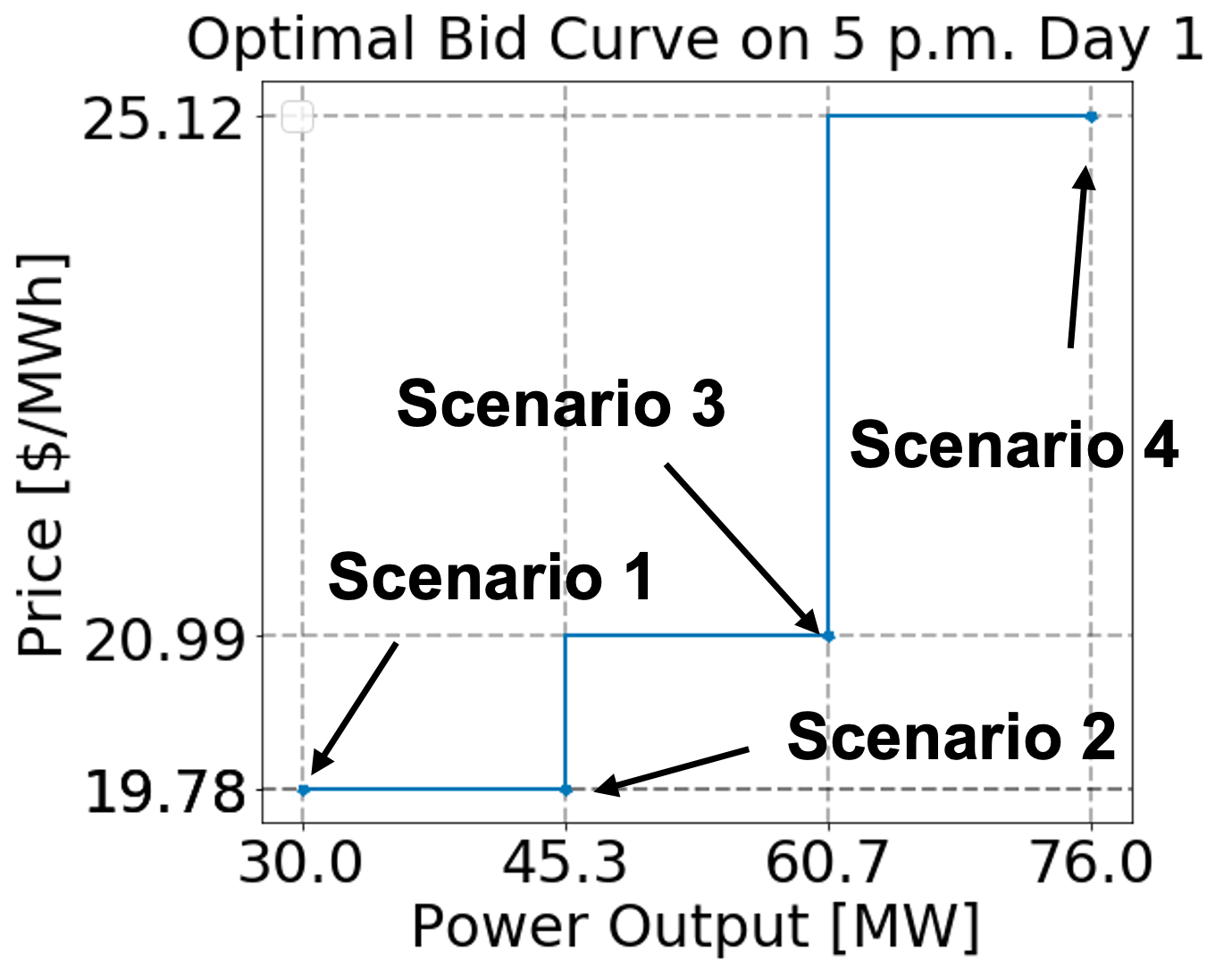

period to communicate their flexibility and marginal costs. As shown in the figure

below, an energy bid is a piecewise constant function described by several energy

offer price ($/MWh) and

operating level (MW) pairs. Bid curves from each resource are inputs (i.e.,

parameters) in the market-clearing optimization problems solved by production cost models. Currently,

the Bidder formulates a two-stage stochastic program to calculate the optimized

time-varying bid curves for thermal generators. In this stochastic program, each

uncertain price scenario has a corresponding power output. As shown in the figure,

each of these uncertain price and power output pairs formulates a segment in the

bidding curves.